Most people go through life earning money, spending money, and hoping things will work out. But the truly wealthy do something different — they track their net worth by age, set clear financial benchmarks, and make deliberate decisions to grow their wealth year after year.

So here is the real question: Are you on track?

Whether you are 22 years old just starting out, 35 trying to catch up, or 50 getting ready for retirement — this 2026 guide will show you exactly where your net worth should be at every age, why most people fall behind, and the specific steps you can take right now to get ahead.

By the end of this article, you will have a clear picture of your financial standing — and a step-by-step plan to improve it. net worth by age

What Is Net Worth? A Simple Explanation

Before we dive into the numbers, let us make sure we are all on the same page. Net worth is one of the most important financial numbers you will ever calculate — yet most people have no idea what theirs is.

Net Worth = Total Assets − Total Liabilities

Assets are everything you own that has financial value:

- Savings and checking accounts

- Investment accounts (stocks, mutual funds, ETFs)

- Retirement accounts (401k, IRA, pension)

- Real estate (current market value of your home or property)

- Vehicles (current resale value)

- Business ownership value

- Other valuable possessions (jewelry, collectibles)

Liabilities are everything you owe to others:

- Mortgage balance

- Student loans

- Car loans

- Credit card debt

- Personal loans

- Medical debt

Here is a simple example: Imagine you have $80,000 in savings and investments, a car worth $15,000, and a retirement account with $40,000. Your total assets are $135,000. But you also have a $60,000 student loan and $10,000 in credit card debt. Your total liabilities are $70,000. That means your net worth is $65,000.

Simple, right? Now let us look at what that number should look like at your age.

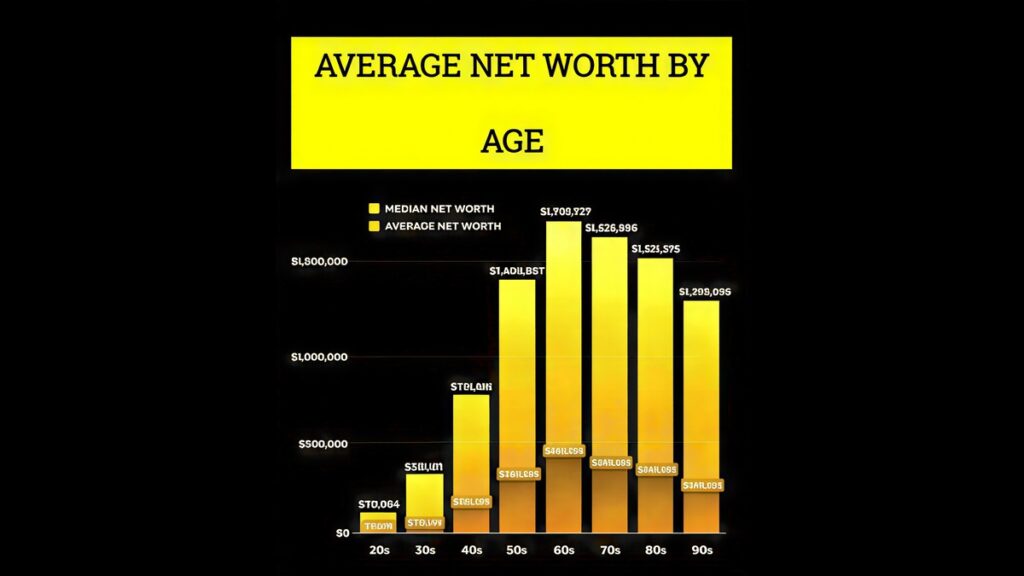

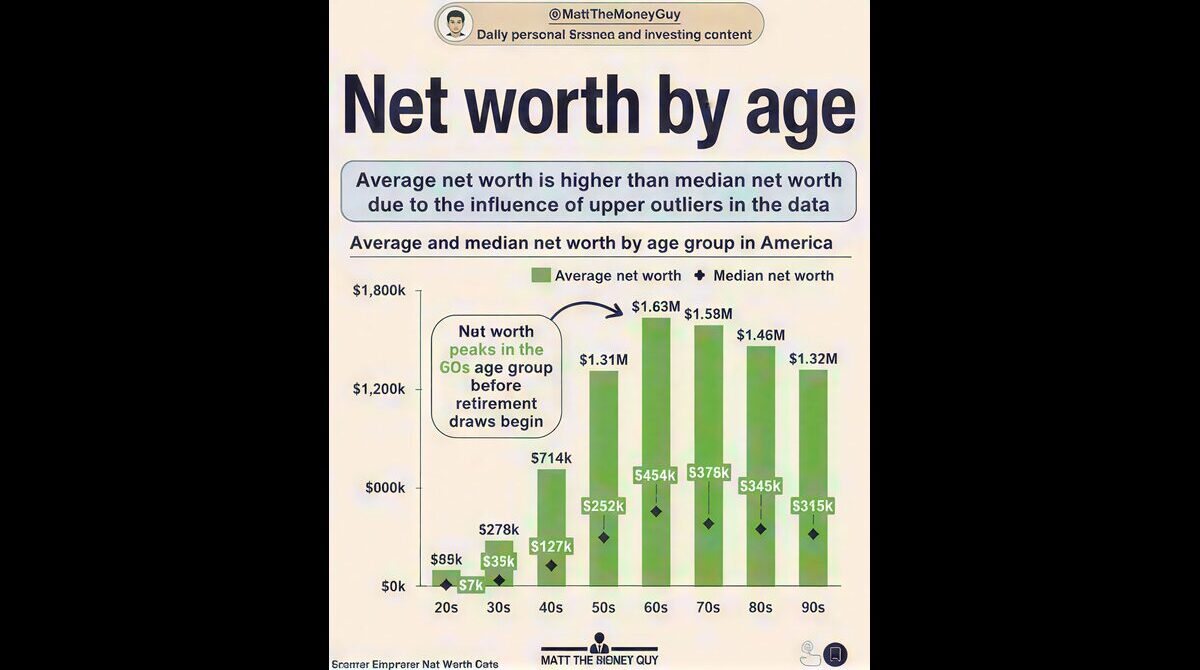

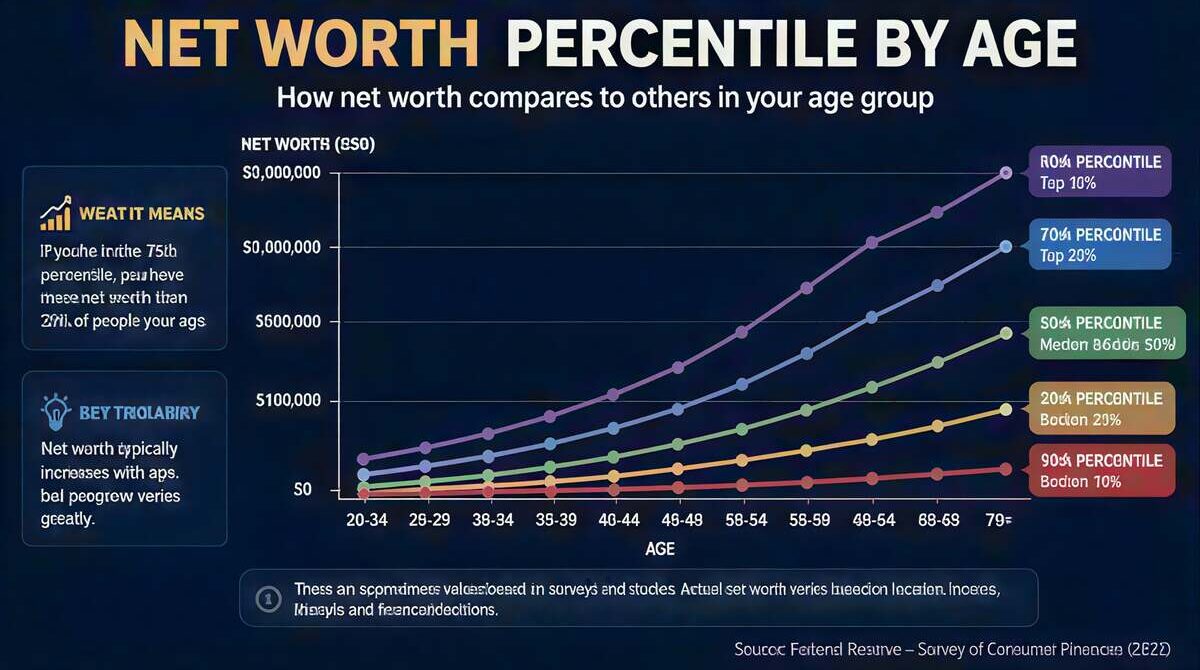

Average Net Worth by Age in 2026 — Full Breakdown

The following table shows the average net worth, a good net worth target, and an ambitious goal for each age group. Use this as your personal financial benchmark.

| Age Group | Average Net Worth | Good Target | Ambitious Goal | Percentile |

| 20–25 | $5,000–$15,000 | $25,000+ | $50,000+ | Top 25% |

| 25–30 | $20,000–$50,000 | $75,000+ | $120,000+ | Top 25% |

| 30–35 | $50,000–$100,000 | $150,000+ | $250,000+ | Top 25% |

| 35–40 | $100,000–$200,000 | $300,000+ | $500,000+ | Top 25% |

| 40–45 | $200,000–$350,000 | $500,000+ | $750,000+ | Top 25% |

| 45–50 | $300,000–$500,000 | $700,000+ | $1,000,000+ | Top 25% |

| 50–55 | $450,000–$700,000 | $900,000+ | $1,300,000+ | Top 25% |

| 55–60 | $600,000–$900,000 | $1,200,000+ | $1,800,000+ | Top 25% |

| 60–65 | $800,000–$1,200,000 | $1,600,000+ | $2,500,000+ | Top 25% |

| 65+ | $1,000,000+ | $2,000,000+ | $3,000,000+ | Top 25% |

These benchmarks are based on general financial planning guidelines. Individual results vary based on income, country, and lifestyle choices.

Net Worth by Age — Detailed Guide for Every Stage of Life

Your 20s (Ages 20–29): Laying the Foundation

Your 20s are arguably the most important decade for your long-term financial future — not because you will accumulate massive wealth, but because the habits you form now will determine your financial fate for the next 40 years.

The reality is that most people in their 20s have a low or even negative net worth. Student loans, entry-level salaries, and the temptation to spend on lifestyle upgrades all make it difficult. But here is the good news: time is your greatest asset. Every dollar you invest in your 20s is worth dramatically more than a dollar invested in your 40s.

The Power of Starting Early: $5,000 invested at age 22, earning 8% annually, grows to over $159,000 by age 65. The same $5,000 invested at age 40 grows to only $43,000. That is the magic of compound interest. How to Boost Your Net Worth 2025

What to Focus on in Your 20s:

- Build an emergency fund first: Save 3 to 6 months of living expenses before anything else. This prevents you from going into debt every time life throws a curveball.

- Attack high-interest debt: Credit card debt at 20% interest is your worst enemy. Pay it off aggressively before investing.

- Start investing immediately — even small amounts: Open a retirement account and invest at least enough to get your employer match if available. Even $100 per month makes a massive difference over time.

- Live below your means: As your income grows, resist the urge to upgrade your lifestyle immediately. Save and invest the difference instead.

- Build your income: Your 20s are the time to invest in education, skills, and career development. Every salary increase should be partially directed to savings and investments.

Net Worth Goal by Age 29: Aim to have a positive net worth of at least $25,000–$50,000. If you have student loans, focus on getting your total liabilities below your total assets.

Your 30s (Ages 30–39): The Wealth Acceleration Decade

Your 30s are when real wealth-building begins. Your income is likely higher than it was in your 20s, your financial habits are more established, and compound interest is starting to work meaningfully in your favor.

However, your 30s also come with major financial pressures: buying a home, raising children, managing a mortgage, and keeping up with peers who seem to be living lavish lifestyles. This is the decade where many people either pull ahead financially or fall dangerously behind.

The 1x Rule: A widely used benchmark is to have your annual salary saved by age 30, and 2x your salary by age 35. If you earn $70,000 per year, you should aim to have $70,000 in net worth by 30 and $140,000 by 35.

What to Focus on in Your 30s:

- Max out retirement contributions: Try to maximize contributions to your 401k, IRA, or other retirement vehicles. Tax-advantaged growth is incredibly powerful.

- Be smart about home buying: Buying a home can be a great wealth builder — but only if you buy within your means. A house that costs more than 3x your annual income can strain your finances severely.

- Diversify your investments: Do not put all your money in one place. Spread across index funds, bonds, and potentially real estate.

- Build multiple income streams: A side business, freelance work, rental income, or dividend investing can dramatically accelerate your net worth growth.

- Protect your wealth: Get adequate life insurance, disability insurance, and a basic will — especially if you have dependents.

Net Worth Goal by Age 39: Aim for $200,000–$300,000 in net worth. If you bought a home, count the equity (home value minus mortgage balance) as part of your net worth.

Your 40s (Ages 40–49): Peak Earning, Peak Building

Your 40s are typically your highest earning years. Career growth, business success, or accumulated professional expertise often lead to significantly higher income. This is the decade where the financial decisions you made in your 20s and 30s really start to show their results.

For some, the 40s bring a financial awakening — suddenly realizing that retirement is only 20 years away and they have not saved enough. For others, it is a time of confident wealth accumulation as their investments compound and their income peaks.

What to Focus on in Your 40s:

- Eliminate all non-mortgage debt: By your mid-40s, you should have zero credit card debt, car loans, and ideally student loans. Debt in your 40s is a serious drag on retirement readiness.

- Increase investment contributions aggressively: With higher income and (hopefully) lower debt, you can significantly increase monthly investing. Even going from $500 to $1,500 per month invested makes an enormous difference.

- Review and rebalance your portfolio: Make sure your investment mix still matches your risk tolerance and timeline. Most 40-somethings should still be heavily invested in stocks.

- Consider real estate investing: If you own your home and have equity, your 40s can be a good time to explore rental property investing as an additional income stream.

- Plan for college costs: If you have children, make sure you have a plan for college funding — but never sacrifice your retirement savings for it.

Net Worth Goal by Age 49: Aim for $500,000–$750,000. At this stage, compound growth becomes very powerful — your investments should be growing significantly on their own.

Your 50s (Ages 50–59): The Final Push Before Retirement

Your 50s are your last major opportunity to build wealth before retirement. This decade is critical. If you are behind on your savings, now is the time to make aggressive changes. If you are on track, now is the time to protect what you have built and fine-tune your retirement plan.

The good news: once you turn 50, you are eligible for catch-up contributions to your retirement accounts, allowing you to save significantly more than younger workers each year.

What to Focus on in Your 50s:

- Maximize catch-up contributions: Take full advantage of higher contribution limits available after age 50 for retirement accounts.

- Visualize your retirement income: Calculate exactly how much income you will need in retirement and whether your current savings will generate it. Use a retirement calculator.

- Start shifting to a more conservative portfolio: Gradually reduce risk in your investment portfolio. You cannot afford a major market crash right before retirement.

- Pay off your mortgage if possible: Entering retirement mortgage-free dramatically reduces your monthly expenses and stress.

- Estimate Social Security or pension benefits: Know what guaranteed income you will have in retirement and plan around it.

Net Worth Goal by Age 59: Aim for $900,000–$1,500,000. At this stage, your goal is to accumulate enough that your investments can generate the income you need for 20-30 years of retirement.

Your 60s and Beyond: Protecting and Enjoying Your Wealth

You made it. Your 60s are about transitioning from wealth-building to wealth-preservation and enjoyment. The financial decisions now focus on making sure your money lasts as long as you do.

What to Focus on in Your 60s:

- Create a sustainable withdrawal strategy: The common rule is to withdraw no more than 4% of your portfolio per year to make it last 30+ years.

- Optimize Social Security timing: Delaying Social Security benefits past age 62 (up to age 70) can significantly increase your monthly benefit.

- Plan for healthcare costs: Healthcare is one of the biggest retirement expenses. Make sure you have adequate coverage and savings for medical needs.

- Consider legacy planning: Update your will, set up trusts if appropriate, and make sure your assets will be distributed according to your wishes.

Why Most People Never Build Significant Net Worth

Understanding why people fail is just as important as knowing what to do. Here are the most common reasons people reach their 40s or 50s with little to no net worth:

- Lifestyle inflation: Every time income increases, spending increases equally or more. The gap between income and expenses — which is where wealth is built — never grows.

- No investment knowledge: Many people leave money sitting in low-interest savings accounts for years, missing out on decades of compound growth.

- Consumer debt: Car payments, credit card balances, and personal loans drain money that could be building wealth. Clara Galle Boyfriend 2025

- No clear financial goals: Without specific targets, spending is emotional rather than strategic.

- Waiting to start: The most expensive financial mistake is waiting. Every year of delay costs thousands of dollars in future wealth.

How to Grow Your Net Worth Faster — 7 Proven Strategies

Strategy 1: Know Your Number — Track Net Worth Monthly

You cannot improve what you do not measure. The single most powerful habit wealthy people have is tracking their net worth regularly. Set up a simple spreadsheet with your assets and liabilities. Update it every month. Watch it grow. This creates accountability and motivation like nothing else. Sajal Aly net worth 2026

Free tools like Personal Capital, Mint, or even a basic Google Sheet can make this effortless. The key is consistency — check your number every single month without fail.

Strategy 2: Close the Gap Between Income and Spending

Net worth grows when you consistently spend less than you earn and invest the difference. Even a modest gap of $300 per month, invested consistently over 30 years at 8% average return, grows to over $440,000. The larger the gap, the faster your wealth grows.

Review your monthly expenses brutally. Identify subscriptions you forgot about, dining habits you can adjust, and discretionary spending that does not bring real value to your life. Every dollar you redirect to investing is a dollar working for your future.

Strategy 3: Invest Consistently and Automatically

The best investment strategy is the one you actually stick to. Set up automatic monthly transfers to your investment accounts so that investing happens before you can spend the money. Index funds that track the broad market have historically returned 7-10% annually over long periods. Wahaj Ali net worth 2026

Do not try to time the market. Do not wait for the perfect moment. Invest every month, regardless of what the market is doing. Time in the market always beats timing the market.

Strategy 4: Eliminate High-Interest Debt Ruthlessly

Carrying credit card debt at 20-25% interest while trying to build wealth is like trying to fill a bathtub with the drain open. High-interest debt must be eliminated as the absolute top priority before serious wealth-building can happen.

Use the debt avalanche method (pay off highest interest rate first) to minimize total interest paid, or the debt snowball method (pay off smallest balance first) to build psychological momentum. Either works — the key is aggressive, consistent action.

Strategy 5: Increase Your Income

There is a limit to how much you can cut expenses — but there is no limit to how much you can earn. Your career is your most valuable financial asset in your 20s, 30s, and 40s. Invest in skills, certifications, and experience that increase your earning power. Hania Aamir Net Worth 2026

Additionally, explore side income sources: freelancing, consulting, an online business, rental income, or dividend investing. Even an extra $500 per month in additional income, invested consistently, creates enormous long-term wealth.

Strategy 6: Build Equity Through Real Estate

Owning a home is not always the right financial decision — but building equity through real estate can be a powerful component of net worth growth. If you own a home, every mortgage payment builds equity. As property values appreciate over time, your net worth grows passively.

For those interested in investment properties, rental real estate can generate monthly cash flow while building equity simultaneously. However, it requires careful analysis and adequate capital reserves to handle vacancies and repairs.

Strategy 7: Protect the Wealth You Build

Building wealth is only half the battle — protecting it is equally important. Adequate insurance coverage (health, life, disability, property) prevents a single catastrophic event from wiping out years of financial progress. An emergency fund of 3-6 months of expenses prevents you from being forced to sell investments at the wrong time.

As your net worth grows, consider working with a fee-only financial advisor to develop a comprehensive wealth protection strategy including proper insurance, estate planning, and tax optimization. Naseem Shah net worth 2026

Frequently Asked Questions About Net Worth by Age

What is a good net worth at 30?

Aim for at least 1x your annual salary. If you earn $60,000 per year, a net worth of $60,000 or more puts you ahead of most people your age.

Is a negative net worth normal in your 20s?

Yes — student loans make this very common. What matters is that your net worth is moving in the right direction every month.

How much net worth do you need to retire comfortably?

Save 25x your annual expenses. If you spend $60,000 per year, you need $1,500,000 — based on the 4% safe withdrawal rule.

Does my home count toward my net worth?

Yes. Add your home equity (market value minus mortgage balance). Just remember — home equity is not cash you can easily spend.

How often should I calculate my net worth?

Monthly is best. It keeps you aware of your progress and helps you catch problems before they get worse.

What is the fastest way to increase net worth?

Earn more, spend less, eliminate high-interest debt, and invest consistently. No shortcuts — just disciplined habits done repeatedly.

Conclusion: Your Net Worth Journey Starts Now

Building wealth is not about luck, inheritance, or getting a perfect life start. It is about making intentional financial decisions consistently over time. The people who achieve significant net worth by any age — whether 30, 40, or 50 — are simply those who started tracking, started saving, and started investing and never stopped.

Here is your three-step action plan starting today:

- Calculate your current net worth. Write down all your assets and liabilities. Know your exact number right now.

- Compare where you are to the benchmarks in this guide. Are you ahead, on track, or behind? Either way, now you know.

- Pick one strategy from this article and implement it this week. Not next month — this week. Open that investment account. Start that emergency fund. Pay extra on that credit card.

Remember this: The best time to start building your net worth was 10 years ago. The second best time is today. No matter where you are right now, you can always improve. The only financial decision you will ever truly regret is the one you kept putting off.

Start today. Track consistently. Stay patient. Your future self will thank you.

){kind=link}

&description=&image=https://infocceleb.com/wp-content/uploads/2026/05/Net-Worth-by-Age-1-1024x576.jpg){kind=link}